When most people think about high income, they assume the challenge is earning more. In reality, that’s rarely the issue. High-income professionals don’t usually have an income problem. They have a tax coordination problem.

This is something we see regularly working with doctors, executives, and business owners across Dallas, Fort Worth, and throughout the country. These are individuals earning substantial incomes, often doing everything they’ve been told to do, maxing retirement accounts, working with a CPA, and making disciplined financial decisions. And yet, despite doing things ‘right,’ they are still giving up significant amounts of wealth to taxes over time—often far more than they realize. Not because they’re careless, but because the system they’re following isn’t coordinated.

At first, this feels counterintuitive. These are thoughtful, capable individuals who are used to making high-level decisions in their careers. The issue isn’t a lack of intelligence or effort. It’s that financial decisions, especially tax decisions, don’t operate in isolation. When each decision is made independently, even good ones can create unintended consequences over time.

I recently recorded a Retirement Blueprint episode on this topic, where I explored how tax inefficiencies build slowly, not from bad decisions, but from disconnected ones. In this article, I want to expand on that idea and walk through where high earners tend to lose meaningful dollars over time, why these patterns are so common, and how to think about taxes more strategically over the long term. Because tax efficiency isn’t about what you pay this year. It’s about what you keep over decades.

Listen on

View the full transcript of the episode here.

Why Do High Earners Still Overpay in Taxes?

One of the biggest misconceptions in financial planning is that tax mistakes come from negligence. In reality, they almost never do. Most high earners are filing correctly, paying on time, and working with qualified professionals. The issue is not execution. It’s scope.

*This illustration is for informational and educational purposes only. Actual outcomes will vary based on individual circumstances.

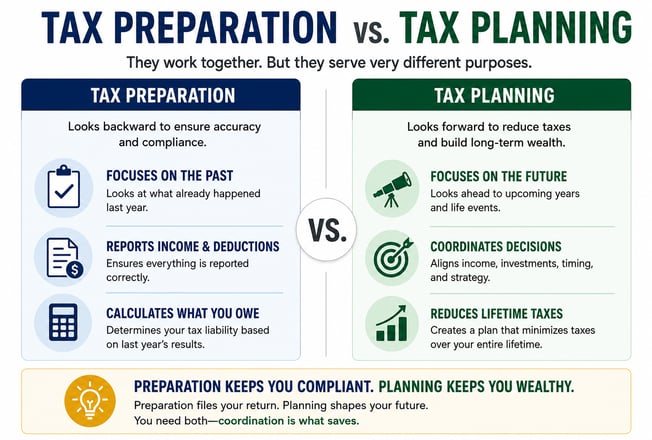

Tax preparation is designed to look backward. It tells you what you owed last year and ensures everything is reported accurately. Tax planning, on the other hand, is forward-looking. It is designed to help evaluate how decisions made today may impact your tax exposure over the next 10, 20, or even 30 years. The problem is that most high earners are only doing half the job. They are focused on compliance, but not coordination. They are optimizing individual years, but not the entire timeline. And that’s where the significant money is lost, quietly, consistently, and often without realizing it.

Why Deferring Taxes Isn’t Always the Right Strategy

For many high earners, the default strategy is to defer as much income as possible. Contributions to 401(k)s, profit-sharing plans, and other pre-tax vehicles reduce taxable income today, which feels efficient and disciplined. In many cases, it is. But deferring taxes doesn’t eliminate them. It simply moves them forward. And when taxes are pushed into the future without a long-term strategy, they may often land in a less favorable environment.  *This illustration is for informational and educational purposes only. Actual outcomes will vary based on individual circumstances.

*This illustration is for informational and educational purposes only. Actual outcomes will vary based on individual circumstances.

Over time, those deferred dollars grow into larger account balances. At the same time, deductions may be reduced, flexibility becomes limited, and income is no longer optional. What started as a smart short-term decision can evolve into a long-term constraint if it isn’t managed intentionally. Deferred dollars don’t disappear. They accumulate. And eventually, the IRS requires that they be withdrawn.

The Risk of Too Much Pre-Tax Money

This is where many high earners run into a problem they didn’t anticipate. After years of disciplined saving, they reach retirement with a large portion of their wealth concentrated in tax-deferred accounts and very little in tax-free or flexible assets. At that point, every withdrawal becomes taxable. Social Security benefits may become taxable. Medicare premiums may increase based on income. Investment income and capital gains begin to stack on top of one another. What once felt manageable starts to compound.

This creates a domino effect. Not because too much was saved, but because everything is taxed the same way. The lack of diversification across tax treatments removes flexibility at the exact time it’s needed most. This isn’t a savings problem. It’s a tax diversification problem.

What Is Tax Diversification, and Why Does It Matter?

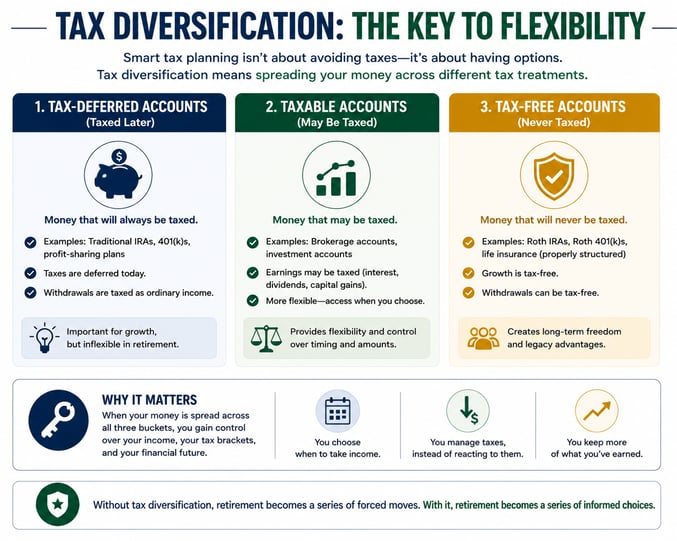

Tax diversification is the concept of spreading your assets across different types of tax treatment. Some assets will always be taxed, such as traditional retirement accounts. Others may be taxed depending on how they are used, like brokerage accounts. And some, like Roth accounts, can provide tax-free income when structured correctly.

*This illustration is for informational and educational purposes only. Actual outcomes will vary based on individual circumstances.

When these buckets are balanced, they create options. You can decide where to pull income from, how much to recognize in a given year, and how to manage your overall tax exposure. Without that balance, retirement becomes far more rigid. Instead of choosing when and how to take income, those decisions are often dictated by external factors like required minimum distributions. And once that happens, flexibility becomes difficult to regain.

Why Marginal Tax Planning Matters More Than Averages

Many high earners focus on their effective tax rate, which represents the average percentage of income paid in taxes. While this can be helpful as a general reference point, it doesn’t drive planning decisions. Planning happens at the margins. It’s the next dollar of income that matters most. That additional dollar can push someone into a higher tax bracket, trigger Medicare surcharges, increase the taxation of Social Security benefits, or phase out valuable deductions.

Two individuals can have the same effective tax rate and still experience very different outcomes based on how their income is structured. Marginal planning is where the most meaningful opportunities, and the costliest mistakes, tend to occur.

How Income Collisions Happen in Retirement

During working years, income is typically predictable and structured. It comes from a salary, bonuses, or equity compensation. In retirement, however, income becomes layered. Required minimum distributions begin. Social Security benefits are added. Investment income and capital gains enter the picture. Each of these sources may seem manageable on its own, but together they can create what is often referred to as tax compression.

When income stacks in this way, it can push retirees into higher tax brackets with limited ability to adjust. At that stage, many of the planning opportunities that existed earlier in life are no longer available. This is why timing plays such a critical role in tax strategy.

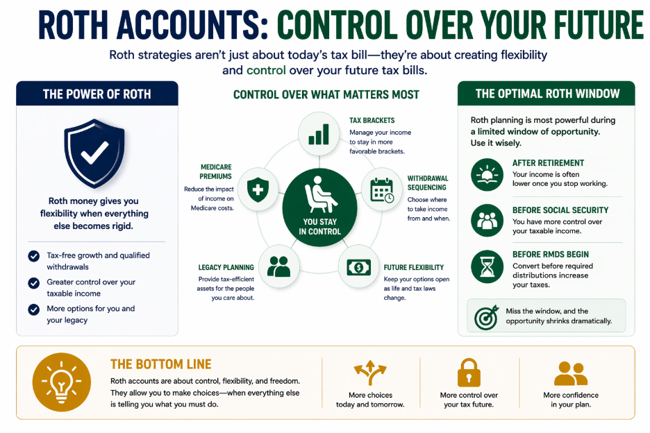

Why Roth Strategies Are Really About Control

Roth accounts are often misunderstood as a short-term tax decision. In reality, they are a long-term control mechanism. Having assets in Roth accounts allows for greater flexibility in how income is managed. It provides options when navigating tax brackets, managing Medicare premiums, and coordinating withdrawals across multiple income sources. It also plays a role in legacy planning by offering tax-efficient assets to future generations. The value of Roth strategies isn’t just in reducing taxes. It’s in creating flexibility when flexibility becomes limited.

*This illustration is for informational and educational purposes only. Actual outcomes will vary based on individual circumstances.

A Real Example: When Timing Changed the Outcome

Consider a representative example of a specialist in his early 50s earning over $600,000 per year. He was disciplined, consistent, and committed to saving aggressively. Every available dollar was directed into pre-tax accounts. From a traditional perspective, everything looked efficient. But when long-term projections were modeled, a different picture emerged.

His required minimum distributions later in life pushed him into higher tax brackets than he experienced during his working years. His Medicare premiums increased, and a larger portion of his Social Security benefits became taxable. Perhaps most importantly, his ability to adjust his income strategy became limited.

He hadn’t made any mistakes. He had simply never coordinated the timing of his decisions. By restructuring when taxes were paid, not how much he earned, hypothetical projections indicated the potential to reduce lifetime tax liability by a meaningful amount, in some cases reaching several hundred thousand dollars, actual results will vary. More importantly, this approach can help improve the flexibility and resilience of his overall plan.

Final Thought

Tax efficiency isn’t about minimizing taxes in a single year. It’s about managing them over time in a way that supports long-term outcomes. High income amplifies both opportunities and mistakes. Without coordination, even well-intentioned strategies can create unnecessary costs. With the right planning, those same decisions can become powerful tools for building flexibility and control. If you want greater confidence in your financial plan, the focus shouldn’t be on finding more deductions. It should be on aligning your decisions across time. Because taxes don’t punish success. They punish unplanned success.

If you would like guidance building a tax strategy that helps coordinate your income, improve long-term tax efficiency, and create greater flexibility across your retirement plan, the team at GDS Wealth Management can help you evaluate where you stand and identify opportunities to strengthen your approach based on your specific situation. Find more information on LinkedIn and YouTube.

GDS Wealth Management is a registered investment adviser. The author is an Investment Adviser Representative of GDS. Registration does not imply a certain level of skill or training. This content is for informational purposes only and is not personalized investment, tax, or legal advice. Any strategies discussed may not be suitable for all individuals and are not guaranteed to produce results. All investments involve risk, including the possible loss of principal, and past performance does not guarantee future results. Examples discussed are hypothetical and for illustrative purposes only and do not represent the experience of any specific client. Any projections or forward-looking statements are hypothetical, based on assumptions, and are not guarantees of future results; actual results will vary materially based on individual circumstances, tax law changes, and other factors, and there is no assurance that any planning strategy will reduce tax liability or improve outcomes. GDS does not provide tax or legal advice; please consult your tax and legal professionals regarding your specific situation. Advisory services are provided pursuant to a written agreement. For additional information about GDS, including its services and fees, please review its Form ADV available at adviserinfo.sec.gov.

{kind=link}